Cost/sell/margin depreciation bond calculation, Cost/sell/margin, Depreciation – Casio ClassPad II fx-CP400 User Manual

Page 185: Bond calculation

Chapter 11

: Financial Application 185

Cost/Sell/Margin

CST

= SEL

100

MRG

1 –

SEL

=

100

MRG

1 –

CST

MRG

(%) =

SEL

CST

1 –

× 100

Depreciation

u Straight-Line Method

YR

1

(PV – FV )

SL

1

=

n

12

×

(PV – FV )

SL

j

=

n

12 – YR1

(YR1 12)

(PV – FV )

n

12

×

SL

n

+1

=

u Fixed-Percentage Method

100

YR

1

I%

FP

1

= PV

×

12

×

100

I%

FP

j

= (RDV

j

–1

+ FV

)

×

FP

n

+1

= RDV

n

(YR1 12)

RDV

1

= PV – FV – FP

1

RDV

j

= RDV

j

–1

– FP

j

RDV

n

+1

= 0 (YR1 12)

u Sum-of-the-Years’-Digits Method

n

(n

+

1)

Z

=

2

2

(Intg (n' ) + 1)(Intg (n' ) + 2

× Frac(n' ) )

Z'

=

SYD

1

=

YR

1

12

n

Z ×

(PV

– FV )

n'

– j + 2

Z'

)(PV

– FV

– SYD

1

)

( j 1)

SYD

j

= (

RDV

1

= PV

– FV

– SYD

1

RDV

j

= RDV

j

–1

– SYD

j

n'

– (n

+

1) + 2

Z'

)(PV

– FV

– SYD

1

)

(YR1 12)

12 – YR1

12

×

SYD

n

+1

= (

12

YR

1

n'

= n –

u Declining-Balance Method

100n

YR

1

I%

DB

1

= PV

×

12

×

RDV

1

= PV – FV – DB

1

100n

I%

×

DB

j

= (RDV

j

–1

+ FV )

RDV

j

= RDV

j

–1

– DB

j

(YR1 12)

DB

n

+1

= RDV

n

(YR1 12)

RDV

n

+1

= 0

Bond Calculation

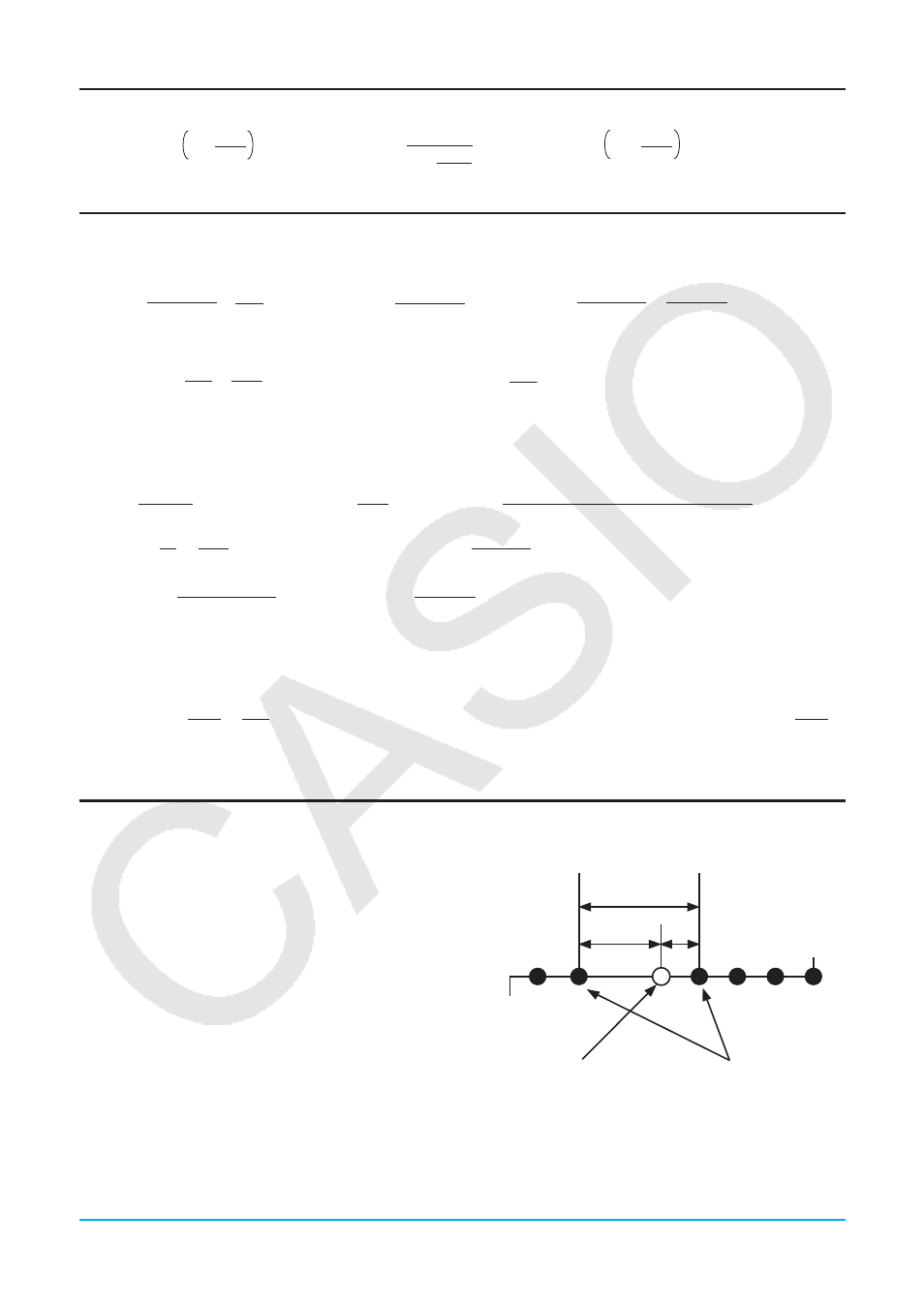

u Terms in the formulas

PRC

: price per $100 of face value

RDV

: redemption price per $100 of face value

CPN

: coupon rate (%)

YLD

: annual yield (%)

M

: number of coupon payments per year

(1 = Annual, 2 = Semi-annual)

N

: number of coupon payments until maturity (

n

is

used when “Term” is specified for “Bond Interval”.)

INT

: accrued interest

CST

: price including interest

A

: accrued days

D

: number of days in coupon period where settlement occurs

B

: number of days from purchase date until next coupon payment date =

D

–

A

D

Issue date

Redemption date (d2)

Purchase date (d1)

Coupon payment dates

A

B