Durbin-watson factor statistics, 40 durbin-watson factor statistics – BUCHI NIRCal User Manual

Page 181

Chemometrics

NIRCal 5.5 Manual, Version A

181

3.18.40

Durbin-Watson Factor Statistics

Description

Statistical test for the determination of the linearity.

Use

Addition information for statistics like regression slope and intercept.

Method

PCR / PLS / Cluster (CLU) / SIMCA

Matrices ID

62

Tip

The C-Set and V-Set selection has a big influence on the Durbin-Watson

value.

Details

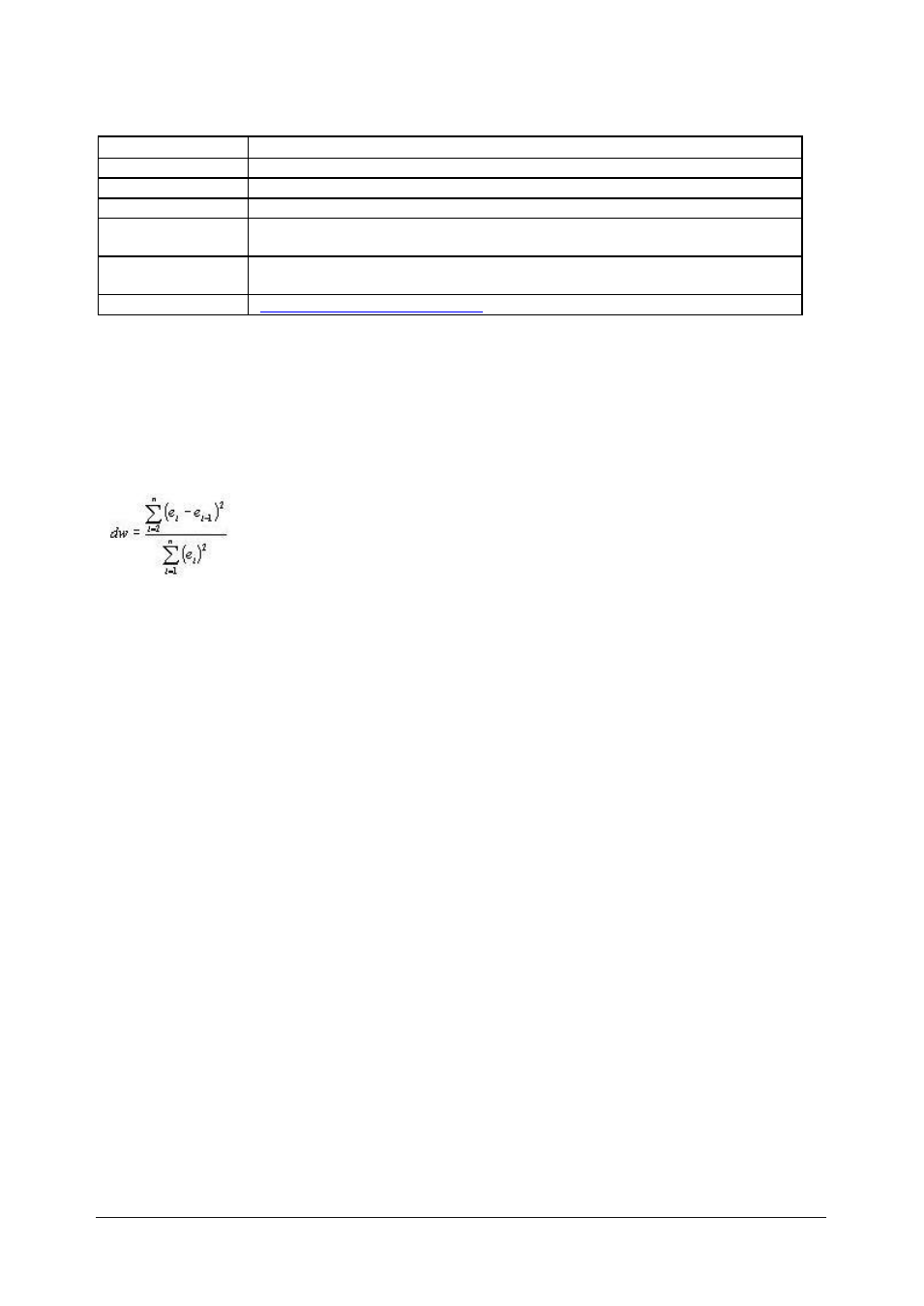

dw = Durbin-Watson = Sum of consecutive/successive Residual Difference

Square / Sum of Residual Square

Related Topic

Calibration Protocol Quantitative

Definition: "The Durbin-Watson test is a test for first-order serial correlation in the residuals of a time

series regression. A value of 2.0 for the Durbin-Watson statistic indicates that there is no serial

correlation. This result is biased toward the finding that there is no serial correlation if lagged values of

the regressors are in the regression.

Formally, the statistic is: d=(sum from t=2 to t=T of: (et-et-1)2/(sum from t=1 to t=T of: et2) where the

series of "et" are the residuals from a regression.

Use Durbin-Watson test to assess correlation between adjacent observations.

e = Property residual = (Original property

– Predicted property)

The Durbin-Watson test checks for sequential dependence in which each error (and also residual) is

correlated with those before and after it in the sequence."

Interpretation:

ranges from 0 (perfect positive correlation) to 4 (perfect negative correlation);

values from 1.5 (= du) to 2.5 (= 4-du) indicate no serious violation of independence ( for n >

30 )

0______1___

1.5__

2

__2.5

___3______4

Results of dw:

0 <= dw <= 4 always;

the distribution of dw is symmetric about 2;

if successive residuals are positively serially correlated, that is positively correlated in their

sequence, dw will be near 0;

if successive residuals are negatively serially correlated, that is negatively correlated in their

sequence, dw will be near 4, so that (4 - dw) will be near 0.

Abbreviation:

dl = dw lower limit;

du = dw upper limit;

k = 1, considering 2 dimensional plots like regression plot;

Residuals from a fittet straigth line Y = b0 + b1* X;

n = number of C-Set resp. V-Set spectra;

alpha = 5% significance, typical;

Limits for dl and du after k, n, alpha are to find in reference:

[Savin, N.E. and White, K.J., "The Durbin-Watson Test for Serial Correlation with Extreme Sample

Sizes or Many Regressors", Econometrica, Vol. 45, 1977, pp. 1989-1996.]

Order : "The observations and residuals have a natural order."