Bonds – Casio ALGEBRA FX2.0 Financial User Manual

Page 24

24

10. Bonds

The bond calculation function calculates the price and yield of a bond.

u

uu

u

u

Formula

PRC

: price per $100 of face value

CPN

: annual coupon rate (%)

YLD

: yield to maturity (%)

A

: accrued days

M

: number of coupon payments per year (1=annual, 2=semi annual)

N

: number of coupon payments between settlement date and maturity date

RDV

: redemption price or call price per $100 of face value

D

: number of days in coupon period where settlement occurs

B

: number of days from settlement date until next coupon payment date = D – A

INT

: accrued interest

CST

: price including interest

• Less than six months to redemption

PRC =

– (

)

RDV

+

M

CPN

1+ (

×

)

D

B

M

YLD/

100

×

D

A

M

CPN

• Six months or more to redemption

–

×

D

A

M

CPN

PRC =

+

RDV

(1+

)

M

YLD/

100

(1+

)

M

YLD/

100

M

CPN

Σ

N

k=1

(

N

–1+

B/D

)

(

K

–1+

B/D

)

–

×

D

A

M

CPN

INT =

CST = PRC

+

INT

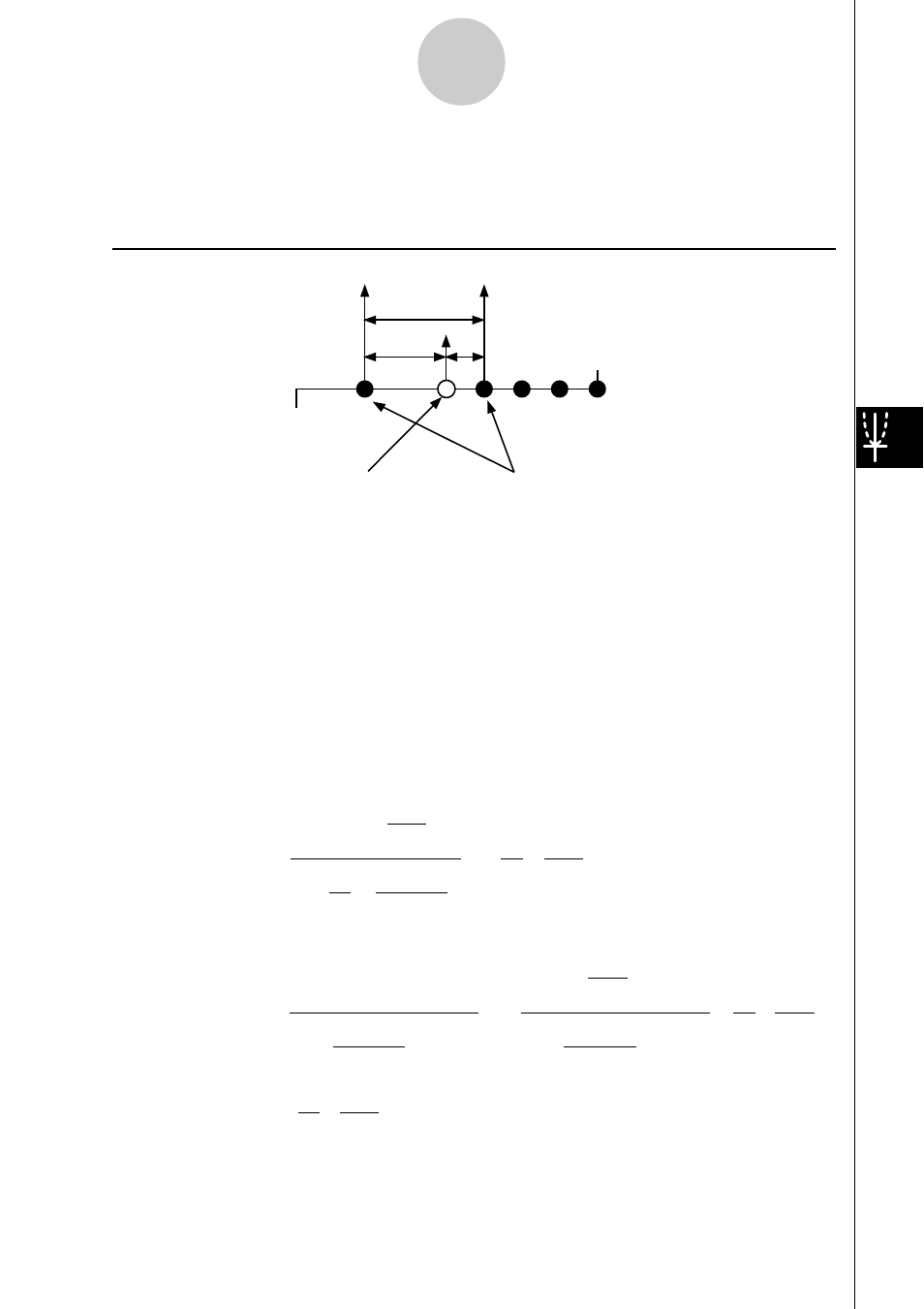

D

Issue date

Redemption date

Purchase date

Coupon Payment dates

A B